Newsletter

Suscríbete a nuestro Newsletter y entérate de las últimas novedades.

https://centrocompetencia.com/wp-content/themes/Ceco

volver

An oligopoly is a market with few companies that are aware of their interdependence in strategic decision-making regarding different variables, such as pricing, production, and quality (European Commission, 2002). This means that each company recognizes that its behavior in the market will clearly affect that of others. As a result, each firm will consider the possible reactions of other competitors.

This means that, in an oligopoly, the number of companies is small enough for each company to have a degree of market power. There is no precise number of firms that defines this structure, but there must be few enough to generate interdependence between companies.

The study of oligopolistic industries lies at the heart of the field of industrial organization. Within market structures, perfect competition and monopoly represent the extremes. Although these are two reference points, empirical evidence suggests that most markets in the real world lie somewhere between these two states. Industries or markets typically have more than one firm, but they do not have the large number of firms assumed in the perfect competition model.

A common aspect of the models of perfect competition and monopoly is that, in both cases, each firm has no reason to be concerned about the actions of others. In the case of monopoly this is obvious, since it is the only firm, while in the case of perfect competition, each firm is so insignificant that its behavior does not have a significant impact on its rivals.

In the real world, by contrast, most companies, when making decisions, must consider how their competitors will respond. In other words, their actions affect other companies and therefore provoke reactions. In economics, these types of relationships are called strategic interactions. Thus, the field of industrial organization studies oligopolies using models in the context of strategic interaction.

Among the topics that the discipline has devoted itself to studying are the determinants of oligopoly prices and quantities, the efficiency of different oligopolistic structures, what determines market power, the conditions that facilitate collusion, the presence of barriers to entry, the role of innovation, among other issues.

Game theory applied to the field of economics examines the strategic behavior of players who interact motivated by utility maximization and who know that the other participants are rational. The goal is to understand what are the strategies that each firm adopts, given that their decisions will affect those of their rivals. The result is a Nash equilibrium, developed by the game theorist and Nobel Prize economist, John Nash.

A Nash equilibrium is reached through a selection of strategies such that no company can improve its position by changing its strategy, given the existing strategies of its rivals. Therefore, a Nash equilibrium represents the best response of any company to the strategies of others.

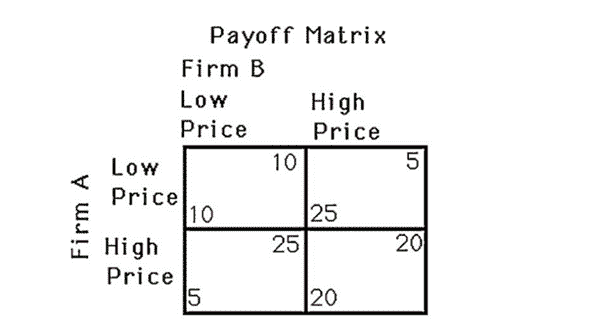

Consider a duopoly, in which each of the two companies chooses a strategy. The pair of strategies chosen is a Nash equilibrium if company A’s choice maximizes its profits, given company B’s choice, and company 2 maximizes its profits, given company 1’s choice.

In the situation shown in the figure, the equilibrium strategy is that in which both firms decide to compete with low prices, since it is the only situation where each player maximizes its profits given the strategy chosen by the rival, and this condition is simultaneously true for both players. Note that if both decide to set a high price, one firm has an incentive to deviate to obtain higher profits at the expense of its rival.

Within oligopoly theory, a distinction is made between models in which companies choose quantities and those in which they choose prices. Quantity-setting models are often referred to as Cournot models, and price-setting models as Bertrand models.

The Cournot oligopoly model assumes that rival companies produce a homogeneous product, and each firm tries to maximize profits by choosing how much to produce. These profits derive from maximum sales volume and higher prices (higher profits). Cournot’s basic assumption is that each company chooses the quantity to produce, taking the quantity of its rivals as given. This interdependence is a problem because increasing profits through higher prices may harm total revenues due to the loss of market share. Thus, equilibrium levels will be the best response of an oligopolist to the production level of its rival firm.

The Cournot model provides equilibrium results that are of great importance for industrial economics. First, in oligopolistic markets, participating firms exercise market power: Cournot’s equilibrium is one where the price exceeds the marginal cost for all participating firms. Second, the equilibrium quantity is higher in Cournot than in the case of monopoly, but lower than in perfect competition. At the same time, the price is lower in Cournot than under monopoly, but not as low as in perfect competition. Third, the greater the number of competitors, the lower their market share and the lower their resulting market power. In other words, as the number of firms increases —decreasing market concentration— the equilibrium approaches what it would be in perfect competition.

In 1883, Bertrand criticized Cournot, arguing that companies in fact choose prices rather than quantities, and that they have very strong incentives to undercut each other’s prices. Thus, the Bertrand oligopoly model emerged. In it, companies independently choose prices in order to maximize profits.

Bertrand’s argument can be summarized as follows: suppose that the market consists of two producers (1 and 2), and producer 1 enters the market first, choosing to charge a price equal to the monopoly price (P1=100). Producer 2, believing that producer 1 will not change its price P1, will set a price slightly lower than P1 (for example, P2 = 99), which will allow it to capture the entire market, as no one will want to buy at a higher price. Producer 1, for its part, will react by setting a price slightly lower than that set by producer 2 (P1 = 98), and so on, the price will continue to fall until an equilibrium is achieved at a price equal to the marginal cost. Note that the equilibrium achieved corresponds to a perfect competition equilibrium, that is, where the price is equal to the marginal cost, and the profits of each company are equal to zero.

The Nash equilibrium for this simple Bertrand game has two important characteristics: (i) Two firms are sufficient to completely eliminate market power, and (ii) Competition between two firms results in the complete dissipation of profits. This result has been called Bertrand’s Paradox, since we do not expect prices in an oligopolistic setting to produce a competitive outcome.

One way to avoid the paradoxes associated with the Bertrand competition model is to assume that goods are differentiated. When products are differentiated, firms understand that they cannot completely undermine their rival and capture the entire market. There will be consumers who prefer the product of firm 1 over that of firm 2, even if the price of firm 1 is higher. As a result, the intensity of price competition is reduced, and both firms exercise market power in equilibrium.

In effect, under differentiation, demand functions of a determined product will depend not only on its own price, but also on the price of the other product. There is interdependence in demand functions: if a producer raises the price slightly, it loses that portion of consumers who do not have a strong preference for its product but retains those who do. Therefore, it moves from having zero profits if the price is equal to marginal cost to having positive profits with a price higher than marginal costs.

Given that competition with perfectly substitutable goods eliminates profits for companies, firms will strive to differentiate their products to increase their profits.

Which model better reflects the real situation faced by companies? The answer is that both Cournot and Bertrand can adequately represent market equilibrium in different industries. Some industries may be better described by the Cournot model, while in other cases Bertrand’s model will be more appropriate.

Consider the case of an industry where production decisions are made in advance, and it is difficult to modify production decisions (in particular, to increase production) in the short term. In such a situation, the Cournot model will be more appropriate to describe the industry. Examples of industries where increasing production can be difficult include heavy goods manufacturing or industries where inventory maintenance is particularly costly. In such cases, each competitor recognizes that its rivals will not be willing to lose sales.

There are other industries where production decisions can be changed quickly. In such cases, the Bertrand model will prove a better approximation. For example, in the video game industry, production is extremely easy due to digital distribution platforms. Bertrand’s model is also more representative of industries where each firm’s production capacity is such that it is possible to supply the entire (or a large part of) market. The case of long-distance telephone companies is a good example of the latter situation.

In summary:

Another way to approach this debate is to consider that both models are, in fact, complementary. Kreps and Scheinkman (1983) were the first to propose a more complex two-stage game in which firms first invest in capacity (competing according to Cournot) and then compete on prices (as in Bertrand).

This model better describes those industries where it is recognized that investment in capacity takes time and cannot be changed quickly in relation to the ease and speed with which prices can be adjusted. In these cases, if one of the firms does not have capacity, the other can raise the price, so Bertrand’s solution would not be obtained. Thus, investing too much in capacity during the first stage leads to more aggressive price competition in the second stage. As a result, both firms have incentives to limit their investments in capacity (below the socially desirable level) to moderate price competition in the second stage.

The authors show that the final equilibrium (in terms of quantity-price) closely resembles the Cournot equilibrium, since, when deciding on their capacity, they know that they will use all of it.

In 1934, Heinrich von Stackelberg proposed a modification of the Cournot model based on the observation that some industries are characterized by the presence of a leading company, in the sense that it commits to its quantity before its competitors. The Stackelberg model is a sequential game —companies no longer make decisions simultaneously— in which a leading company chooses the quantity and then, after observing the leader’s quantity, the follower firm chooses its quantity.

The relevant aspect of this model, which incorporates sequentiality, is that now the company that acts first —the leading company— has an advantage because it is the first player, allowing it to anticipate the possible strategies of the follower firm. Thus, Stackelberg equilibrium differs from Cournot equilibrium, where total production is higher and prices are lower, but the leading firm comes out better. This model therefore highlights the importance of market information when defining a strategy.

A dominant firm is one that possesses a significant share of a given market and has a considerably larger market share than its next largest rival. Therefore, an industry with a dominant firm is often an oligopoly as there is a small number of firms. However, it is an asymmetric oligopoly, because the firms are not the same size. Dominant firms are generally considered to have market shares of 40% or more.

Typically, the dominant firm faces a series of small competitors, known as the competitive fringe, whose effect is to dampen, but not eliminate, the dominant firm’s control over price. It is usually assumed that the dominant firm has some competitive advantage over the fringe. The result of this model is that, in the presence of a competitive fringe, the demand received by the dominant firm is more elastic and, therefore, the situation resembles that of a monopoly facing residual (reduced) demand as a result of the competitive fringe, resulting in equilibrium prices lower than those of a strict monopoly. Dominant firms may be of concern to competition policy when they achieve or maintain their dominant position as a result of anticompetitive practices (see the glossary Abuse of dominant position).

If the dominant firm decides to raise prices, it may end up affecting its profits, since, on the one hand, price increases cause the supply from small firms to increase, which leads to a reduction in the residual demand faced by the dominant firm and, on the other hand, the quantity demanded always decreases as the price increases. Thus, the dominant firm will tend to lower the price (relative to the monopoly case) to reduce the supply of small firms.

On April 24, 1996, the European Commission (hereinafter, the “Commission”) prohibited the merger between Gencor, a South African conglomerate specializing in the production of metals and minerals, and Lonrho, a British company active in the mining and refining sectors, after concluding that the transaction would consolidate a duopoly in the global platinum production market.

Prior to the merger, the platinum market was dominated by three large South African producers: Amplats, Implats, and LPD, which together controlled approximately 90% of global reserves. The proposed merger involved combining Implats and LPD under the joint control of Gencor and Lonrho, reducing the number of major players in the market from three to only two.

According to the Commission’s findings, the platinum market had many characteristics typical of an oligopoly: a small number of competitors, a homogeneous product, high transparency —both in terms of prices and quantities— and high barriers to entry. Thus, in the scenario proposed by the merger, with only two dominant companies of similar size and structure, incentives to compete were significantly reduced, while the risk of tacit coordination increased. This was to the detriment of consumers and the competitive functioning of the market.

In effect, the strategic interdependence between companies, a central feature of oligopolistic markets, was intensified because of the operation. The Commission noted that in markets such as platinum, where companies can easily observe the prices and quantities offered by their competitors, it is natural for them to adjust their own strategic decisions based on the behavior of others. This facilitates the emergence of scenarios of conscious parallelism, in which each firm avoids competing aggressively so as not to provoke retaliation from its rivals, without the need to establish explicit agreements.

Bertrand, J. (1883). Théorie mathématique de la richesse sociale. Journal des savants, 67(1883), 499-508.

Church, J. R., & Ware, R. (2000). Classic Models of Oligopoly. Industrial organization: a strategic approach (pp. 231-274). Homewood, IL.: Irwin McGraw Hill.

European Commission. Glossary of terms used in EU competition policy–antitrust and control of concentrations. Luxembourg: Office for Official Publications of the European Communities, 2002.

Khemani, R. S. (1993). Glossary of industrial organisation economics and competition law. Organisation for Economic Co-operation and Development; Washington, DC: OECD Publications and Information Centre.

Kreps, D. M., & Scheinkman, J. A. (1983). Quantity precommitment and Bertrand competition yield Cournot outcomes. The Bell Journal of Economics, 326-337.

Tirole, J., & Jean, T. (1988). Short-Run Price Competition. The theory of industrial organization (pp. 209-223). MIT press.

Von Stackelberg, H. (1934). Marktform und gleichgewicht. J. springer.